MCMC et inférence bayésienne computationnelle#

Quand le posterior est trop complexe pour être calculé, on l’échantillonne.

Introduction : pourquoi le MCMC ?#

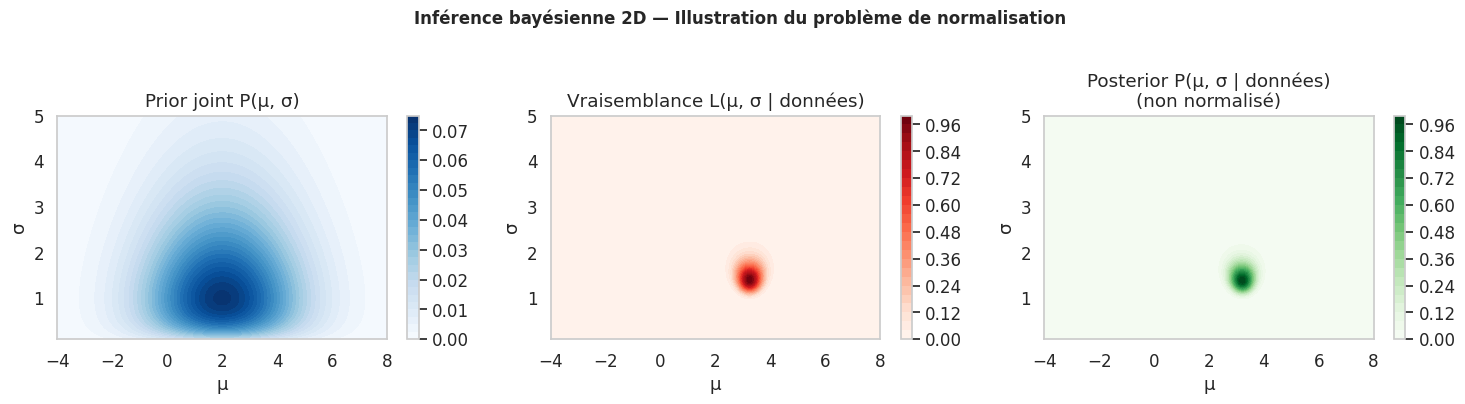

Le chapitre précédent a montré que l’inférence bayésienne requiert de calculer la distribution posterior :

Le problème est le dénominateur : l”evidence \(P(\mathbf{y})\) est une intégrale en dimension \(d\) (le nombre de paramètres). Pour des modèles réalistes avec des priors non-conjugués ou des structures hiérarchiques, cette intégrale est analytiquement intractable et le coût de l’intégration numérique croît exponentiellement avec \(d\).

Les méthodes MCMC (Markov Chain Monte Carlo) contournent ce problème en construisant une chaîne de Markov dont la distribution stationnaire est précisément le posterior souhaité. On n’a pas besoin de normaliser !

Chaînes de Markov : rappels#

Une chaîne de Markov est une suite de variables aléatoires \(\theta^{(1)}, \theta^{(2)}, \ldots\) telle que l’état suivant ne dépend que de l’état courant (propriété de Markov) :

Pour que la chaîne converge vers le posterior cible \(\pi(\theta)\), elle doit être :

Irréductible : tout état est accessible depuis tout autre état

Apériodique : la chaîne ne s’enferme pas dans des cycles

Réversible : condition de bilan détaillé \(\pi(\theta) q(\theta \to \theta') = \pi(\theta') q(\theta' \to \theta)\)

Algorithme de Metropolis-Hastings#

L’algorithme de Metropolis-Hastings (MH) est le fondement de la plupart des méthodes MCMC. Il construit une chaîne en proposant un nouveau point \(\theta^*\) et en l’acceptant ou le rejetant selon un ratio.

Algorithme :

Initialiser \(\theta^{(0)}\) arbitrairement

Pour \(t = 1, 2, \ldots, T\) :

Proposer \(\theta^* \sim q(\theta^* \mid \theta^{(t-1)})\)

Calculer le ratio d’acceptation : \(\alpha = \min\left(1, \frac{\pi(\theta^*) \, q(\theta^{(t-1)} \mid \theta^*)}{\pi(\theta^{(t-1)}) \, q(\theta^* \mid \theta^{(t-1)})}\right)\)

Accepter avec probabilité \(\alpha\) : \(\theta^{(t)} = \theta^*\) ; sinon \(\theta^{(t)} = \theta^{(t-1)}\)

Astuce clé : travail en log

En pratique, le ratio est calculé en log pour éviter les sous-débordements numériques : \(\log \alpha = \log \pi(\theta^*) - \log \pi(\theta^{(t-1)}) + \log q(\theta^{(t-1)}|\theta^*) - \log q(\theta^*|\theta^{(t-1)})\)

Pour une marche aléatoire gaussienne (proposition symétrique), les termes \(q\) s’annulent.

Implémentation complète from scratch#

Exemple : inférence de la moyenne et variance d’une Normale#

def log_prior(mu, log_sigma):

"""Log-prior : mu ~ N(0,10), log(sigma) ~ N(0,1)."""

lp_mu = norm.logpdf(mu, 0, 10)

lp_logsigma = norm.logpdf(log_sigma, 0, 1)

return lp_mu + lp_logsigma

def log_likelihood(data, mu, log_sigma):

"""Log-vraisemblance gaussienne."""

sigma = np.exp(log_sigma)

return np.sum(norm.logpdf(data, mu, sigma))

def log_posterior(data, mu, log_sigma):

"""Log-posterior non normalisé."""

return log_prior(mu, log_sigma) + log_likelihood(data, mu, log_sigma)

def metropolis_hastings(data, n_iter=10000, step_size=0.15, seed=42):

"""

Metropolis-Hastings avec marche aléatoire gaussienne.

Paramètres : (mu, log_sigma) pour estimer N(mu, sigma²).

"""

rng = np.random.default_rng(seed)

# Initialisation

theta_curr = np.array([0.0, 0.0]) # (mu, log_sigma)

lp_curr = log_posterior(data, theta_curr[0], theta_curr[1])

chain = np.zeros((n_iter, 2))

accepted = 0

for t in range(n_iter):

# Proposition : marche aléatoire gaussienne

theta_prop = theta_curr + rng.normal(0, step_size, 2)

lp_prop = log_posterior(data, theta_prop[0], theta_prop[1])

# Ratio d'acceptation (log-espace)

log_alpha = lp_prop - lp_curr

log_u = np.log(rng.uniform())

if log_u < log_alpha:

theta_curr = theta_prop

lp_curr = lp_prop

accepted += 1

chain[t] = theta_curr

taux_accept = accepted / n_iter

return chain, taux_accept

# Génération des données

np.random.seed(2024)

true_mu, true_sigma = 3.7, 1.4

data_mh = np.random.normal(true_mu, true_sigma, 50)

print(f"Vraies valeurs : μ = {true_mu}, σ = {true_sigma}")

print(f"Statistiques empiriques : ȳ = {data_mh.mean():.3f}, s = {data_mh.std():.3f}")

# Lancer MCMC

chain, taux = metropolis_hastings(data_mh, n_iter=15000, step_size=0.15)

chain_mu = chain[:, 0]

chain_sigma = np.exp(chain[:, 1]) # retour en espace σ

print(f"\nTaux d'acceptation : {taux:.1%}")

print(f"(Idéal : 20-40% pour marche aléatoire)")

Vraies valeurs : μ = 3.7, σ = 1.4

Statistiques empiriques : ȳ = 3.700, s = 1.342

Taux d'acceptation : 50.1%

(Idéal : 20-40% pour marche aléatoire)

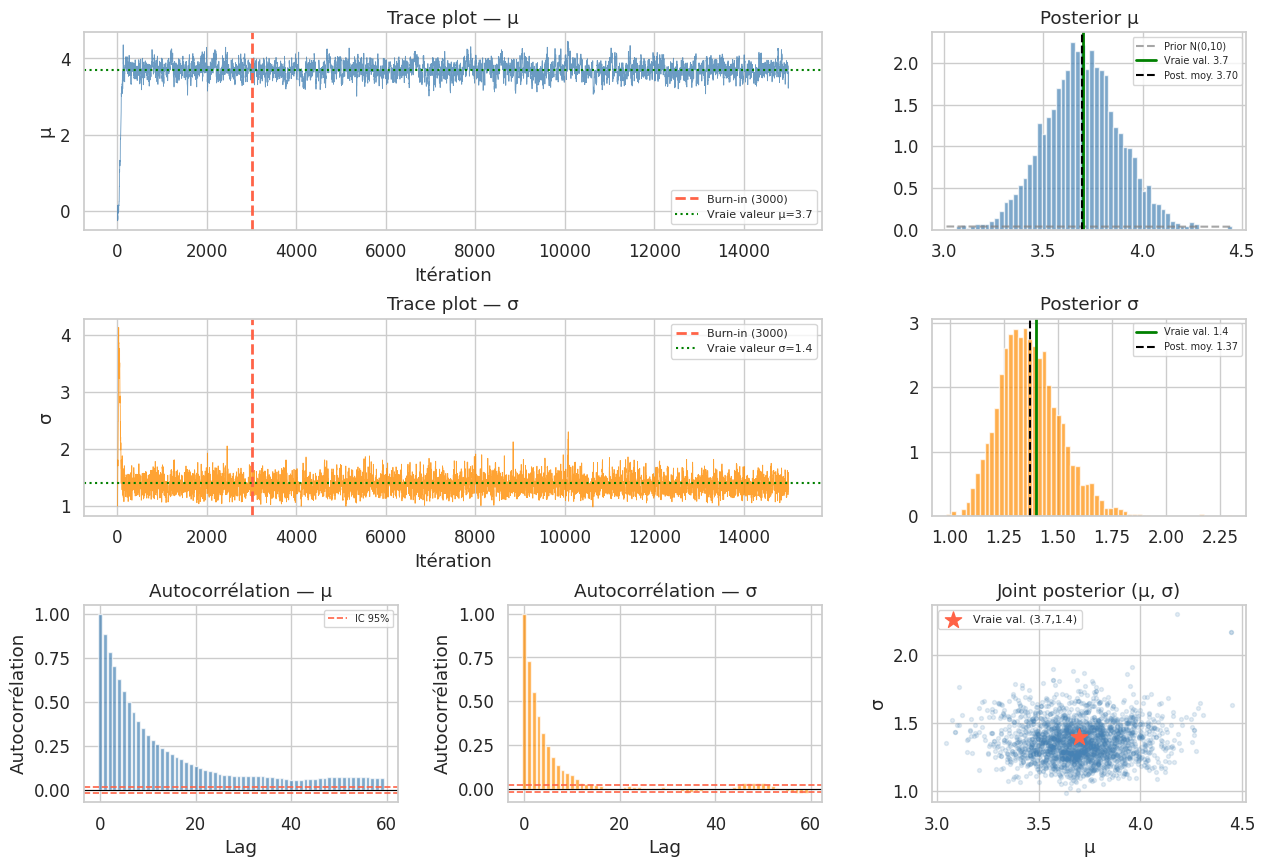

# Résultats après burn-in

burn_in = 3000

chain_mu_post = chain_mu[burn_in:]

chain_sigma_post = chain_sigma[burn_in:]

print("Inférence bayésienne (MCMC) :")

print(f" μ — Moyenne : {chain_mu_post.mean():.3f} "

f"IC 95% : [{np.percentile(chain_mu_post, 2.5):.3f}, {np.percentile(chain_mu_post, 97.5):.3f}]")

print(f" σ — Moyenne : {chain_sigma_post.mean():.3f} "

f"IC 95% : [{np.percentile(chain_sigma_post, 2.5):.3f}, {np.percentile(chain_sigma_post, 97.5):.3f}]")

print(f"\nVraies valeurs : μ = {true_mu}, σ = {true_sigma}")

Inférence bayésienne (MCMC) :

μ — Moyenne : 3.696 IC 95% : [3.316, 4.081]

σ — Moyenne : 1.370 IC 95% : [1.125, 1.680]

Vraies valeurs : μ = 3.7, σ = 1.4

Diagnostics MCMC#

Taux d’acceptation#

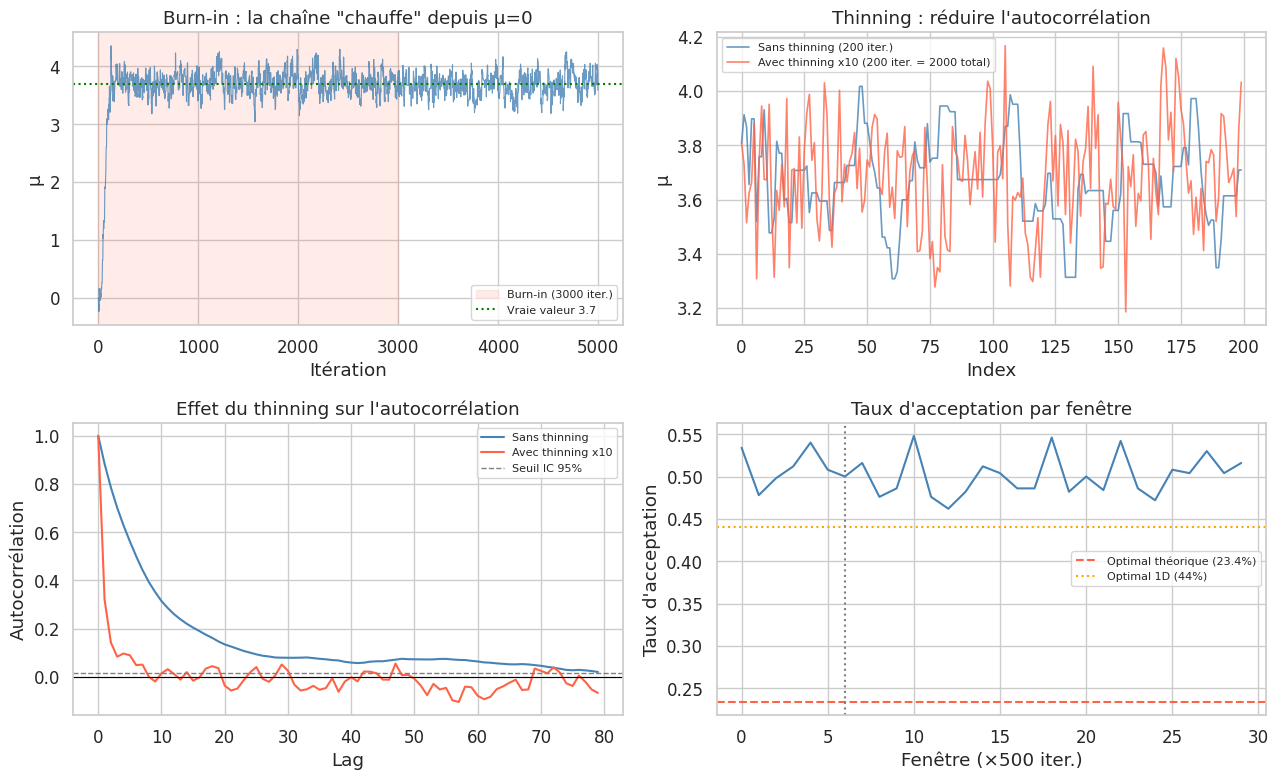

# Effet de la taille de pas sur le taux d'acceptation

step_sizes = [0.01, 0.05, 0.1, 0.2, 0.5, 1.0, 2.0]

results_steps = []

for step in step_sizes:

chain_test, taux_test = metropolis_hastings(data_mh, n_iter=5000, step_size=step, seed=1)

chain_test_post = chain_test[1000:, 0]

results_steps.append({

'step_size': step,

'taux_acceptation': taux_test,

'ESS_approx': len(chain_test_post) / (1 + 2 * sum(

[np.corrcoef(chain_test_post[:-l], chain_test_post[l:])[0, 1]

for l in range(1, min(50, len(chain_test_post)//4))]

))

})

df_steps = pd.DataFrame(results_steps)

print("Effet de la taille de pas :")

print(df_steps.to_string(index=False))

print("\n→ Taux optimal : 20-40% (balance exploration/exploitation)")

Effet de la taille de pas :

step_size taux_acceptation ESS_approx

0.01 0.9060 40.496172

0.05 0.8072 74.084814

0.10 0.6460 201.818813

0.20 0.3918 419.631522

0.50 0.1142 209.168353

1.00 0.0320 105.754691

2.00 0.0092 49.513696

→ Taux optimal : 20-40% (balance exploration/exploitation)

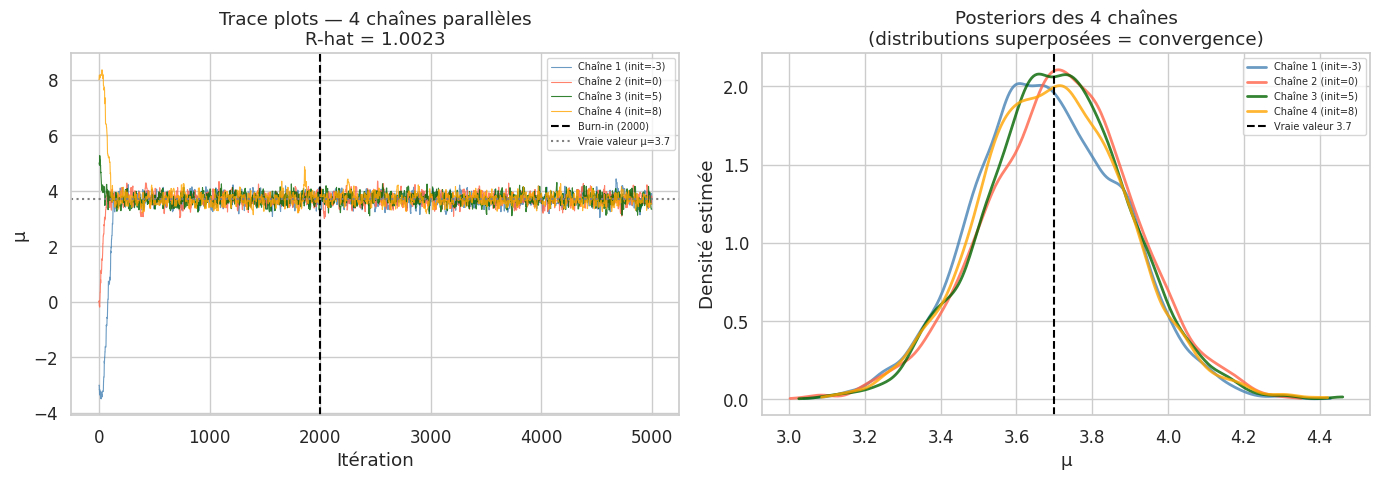

R-hat (Gelman-Rubin)#

Le diagnostic de Gelman-Rubin (\(\hat{R}\)) compare la variance entre plusieurs chaînes et la variance intra-chaîne. Une valeur proche de 1 indique la convergence.

def gelman_rubin(chains):

"""

Calcule R-hat de Gelman-Rubin pour plusieurs chaînes.

chains : liste de tableaux 1D de même longueur.

"""

M = len(chains) # nombre de chaînes

N = len(chains[0]) # longueur (après burn-in)

chain_means = np.array([c.mean() for c in chains])

overall_mean = chain_means.mean()

# Variance entre chaînes

B = N / (M - 1) * np.sum((chain_means - overall_mean) ** 2)

# Variance intra-chaînes

W = np.mean([c.var(ddof=1) for c in chains])

# Variance marginale estimée

var_hat = (1 - 1/N) * W + B/N

R_hat = np.sqrt(var_hat / W)

return R_hat

# Lancer 4 chaînes avec initialisations différentes

chains_mu = []

for seed_i, init_mu in zip([42, 123, 456, 789], [-3, 0, 5, 8]):

def mh_init(data, init, n_iter=8000, step_size=0.2, seed=42):

rng = np.random.default_rng(seed)

theta_curr = np.array([init, 0.0])

lp_curr = log_posterior(data, theta_curr[0], theta_curr[1])

chain = np.zeros((n_iter, 2))

for t in range(n_iter):

theta_prop = theta_curr + rng.normal(0, step_size, 2)

lp_prop = log_posterior(data, theta_prop[0], theta_prop[1])

if np.log(rng.uniform()) < lp_prop - lp_curr:

theta_curr = theta_prop

lp_curr = lp_prop

chain[t] = theta_curr

return chain

ch = mh_init(data_mh, init_mu, seed=seed_i)

chains_mu.append(ch[2000:, 0]) # après burn-in

R_hat = gelman_rubin(chains_mu)

print(f"R-hat (Gelman-Rubin) pour μ : {R_hat:.4f}")

print(f"→ R-hat < 1.01 : convergence excellente")

print(f"→ R-hat < 1.05 : convergence acceptable")

print(f"→ R-hat > 1.1 : chaîne non convergée — augmenter n_iter")

R-hat (Gelman-Rubin) pour μ : 1.0023

→ R-hat < 1.01 : convergence excellente

→ R-hat < 1.05 : convergence acceptable

→ R-hat > 1.1 : chaîne non convergée — augmenter n_iter

Taille effective d’échantillon (ESS)#

L’autocorrélation réduit l’information effective de la chaîne. L’ESS (Effective Sample Size) estime le nombre d’échantillons indépendants équivalents :

def ess(chain, max_lag=200):

"""Calcule l'ESS par la somme des autocorrélations."""

n = len(chain)

rho_sum = 0

for lag in range(1, min(max_lag, n//4)):

rho = np.corrcoef(chain[:-lag], chain[lag:])[0, 1]

if rho < 0.05: # stop quand autocorr négligeable

break

rho_sum += rho

return n / (1 + 2 * rho_sum)

ess_mu = ess(chain_mu_post)

ess_sigma = ess(chain_sigma_post)

n_post = len(chain_mu_post)

print(f"Taille de la chaîne (après burn-in) : {n_post}")

print(f"ESS pour μ : {ess_mu:.0f} ({ess_mu/n_post:.1%} d'efficacité)")

print(f"ESS pour σ : {ess_sigma:.0f} ({ess_sigma/n_post:.1%} d'efficacité)")

print(f"\n→ ESS > 400 est généralement suffisant pour estimer la moyenne et l'IC 95%.")

Taille de la chaîne (après burn-in) : 12000

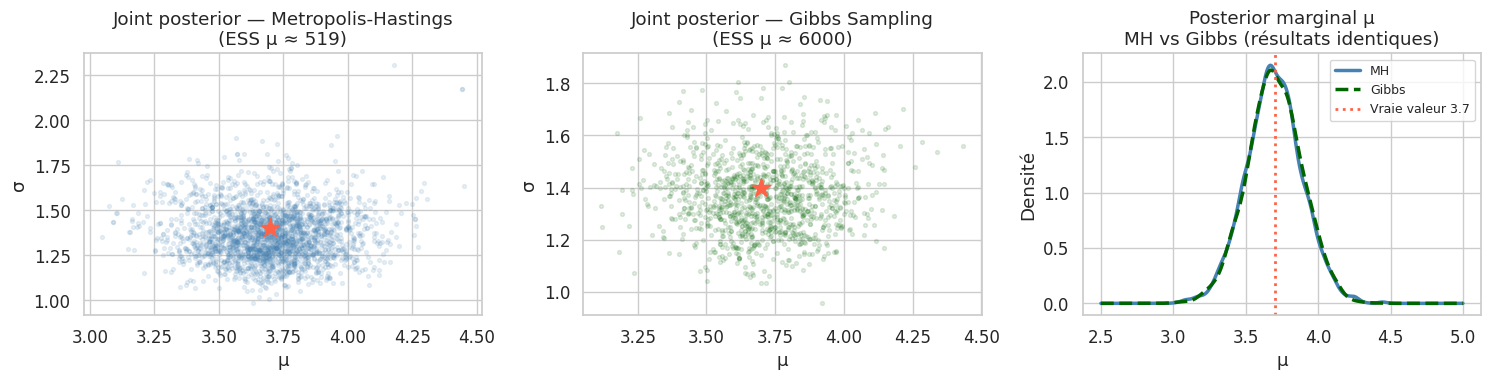

ESS pour μ : 519 (4.3% d'efficacité)

ESS pour σ : 1762 (14.7% d'efficacité)

→ ESS > 400 est généralement suffisant pour estimer la moyenne et l'IC 95%.

Burn-in et thinning#

Gibbs Sampling#

Le Gibbs sampling est un cas particulier de MH où l’on tire chaque paramètre depuis sa distribution conditionnelle complète, en fixant tous les autres. Taux d’acceptation = 100%.

def gibbs_sampler_normal(data, n_iter=8000, seed=42):

"""

Gibbs sampler pour N(mu, sigma²) avec priors conjugués :

mu | sigma² ~ N(mu0, tau0²)

sigma² ~ InvGamma(a0, b0)

"""

rng = np.random.default_rng(seed)

n = len(data)

y_bar = np.mean(data)

# Hyperparamètres des priors

mu0, tau0_sq = 0.0, 100.0 # prior sur mu

a0, b0 = 0.1, 0.1 # prior sur sigma² (quasi non-informatif)

# Initialisation

mu_curr = y_bar

sigma2_curr = np.var(data, ddof=1)

chain_gibbs = np.zeros((n_iter, 2))

for t in range(n_iter):

# 1. Tirer mu | sigma², données

tau_n_sq = 1 / (1/tau0_sq + n/sigma2_curr)

mu_n = tau_n_sq * (mu0/tau0_sq + n*y_bar/sigma2_curr)

mu_curr = rng.normal(mu_n, np.sqrt(tau_n_sq))

# 2. Tirer sigma² | mu, données

a_n = a0 + n/2

b_n = b0 + 0.5 * np.sum((data - mu_curr)**2)

sigma2_curr = 1 / rng.gamma(a_n, 1/b_n) # InvGamma via Gamma

chain_gibbs[t] = [mu_curr, np.sqrt(sigma2_curr)]

return chain_gibbs

chain_gibbs = gibbs_sampler_normal(data_mh, n_iter=8000)

burn_gibbs = 2000

chain_g_mu = chain_gibbs[burn_gibbs:, 0]

chain_g_sigma = chain_gibbs[burn_gibbs:, 1]

print("Résultats Gibbs Sampling :")

print(f" μ : {chain_g_mu.mean():.3f} "

f"IC 95% : [{np.percentile(chain_g_mu, 2.5):.3f}, {np.percentile(chain_g_mu, 97.5):.3f}]")

print(f" σ : {chain_g_sigma.mean():.3f} "

f"IC 95% : [{np.percentile(chain_g_sigma, 2.5):.3f}, {np.percentile(chain_g_sigma, 97.5):.3f}]")

print(f"\nVraies valeurs : μ = {true_mu}, σ = {true_sigma}")

print(f"ESS μ (Gibbs) : {ess(chain_g_mu):.0f}")

print(f"ESS μ (MH) : {ess(chain_mu_post):.0f}")

Résultats Gibbs Sampling :

μ : 3.700 IC 95% : [3.319, 4.073]

σ : 1.373 IC 95% : [1.127, 1.677]

Vraies valeurs : μ = 3.7, σ = 1.4

ESS μ (Gibbs) : 6000

ESS μ (MH) : 519

Mentions : PyMC et approximation variationnelle#

PyMC (non installé dans cet environnement)

PyMC est la bibliothèque Python de référence pour la modélisation bayésienne probabiliste. Elle fournit une interface de haut niveau pour spécifier des modèles et utilise des algorithmes avancés comme NUTS (No-U-Turn Sampler, une variante adaptative de HMC).

Exemple de syntaxe PyMC pour le même modèle :

import pymc as pm

with pm.Model() as model:

mu = pm.Normal('mu', mu=0, sigma=10)

sigma = pm.HalfNormal('sigma', sigma=1)

y_obs = pm.Normal('y_obs', mu=mu, sigma=sigma, observed=data)

trace = pm.sample(2000, tune=1000, chains=4, return_inferencedata=True)

pm.plot_trace(trace)

Approximation variationnelle (VI)

L”inférence variationnelle remplace l’échantillonnage par un problème d’optimisation : on cherche la distribution \(q(\theta)\) dans une famille paramétrique (ex : Gaussienne) qui minimise la divergence KL avec le posterior. Plus rapide que MCMC mais l’approximation peut être inexacte pour des posteriors complexes ou multimodaux. Implémentée dans PyMC (pm.fit()), TensorFlow Probability, et Pyro.

Résumé#

Points clés — MCMC

Le MCMC permet d’échantillonner des posteriors sans calculer la constante de normalisation.

Metropolis-Hastings : algorithme général, taux d’acceptation cible 20-40% pour une marche aléatoire.

Gibbs Sampling : efficace quand les conditionnelles complètes sont disponibles, taux d’acceptation 100%.

Diagnostics indispensables : trace plots (chaîne mixée ?), R-hat < 1.01 (convergence ?), ESS > 400 (précision ?), autocorrélation (nécessité de thinning ?).

Burn-in : jeter les premières itérations pendant la phase de « chauffe ».

En pratique, utiliser PyMC ou Stan qui implémentent des algorithmes plus efficaces (NUTS/HMC).